Topics

Why Talk About Money?

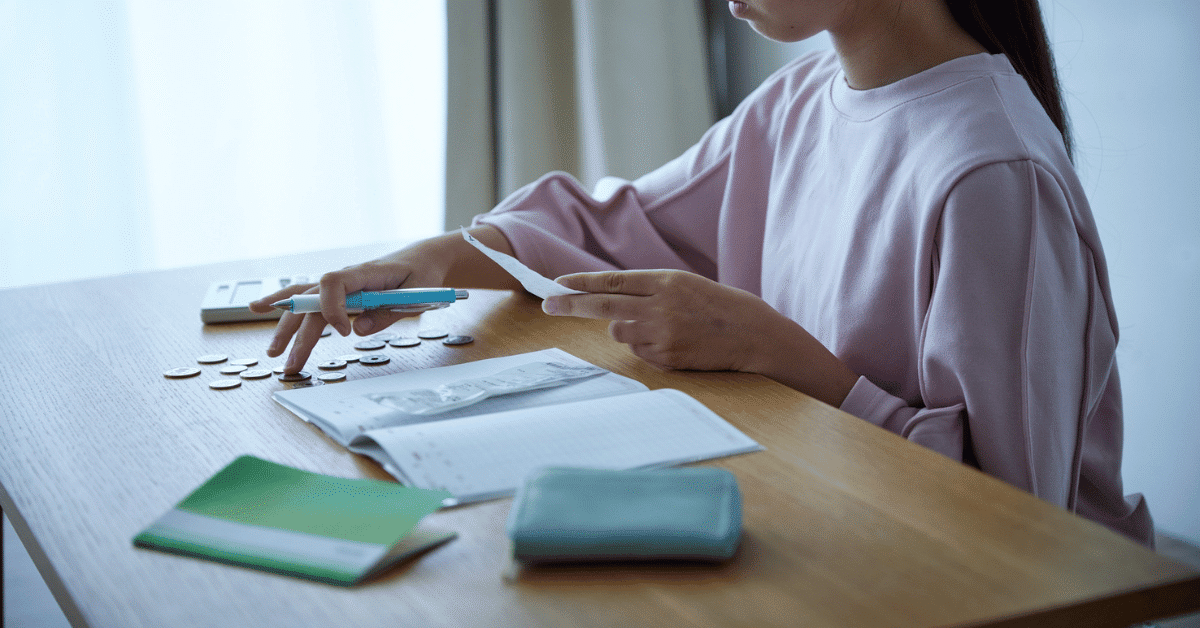

Talking about money is still taboo for many people. Whether out of shame, lack of knowledge, or simply finding the subject complicated, we often avoid facing the reality of our finances. However, ignoring the importance of personal financial organization is like navigating a stormy sea without a compass: you might stay afloat for a while, but you’ll hardly reach your desired destination. In this article, we’ll demystify financial organization, showing why it’s crucial not just for getting out of debt, but for building a more secure and peaceful future.

Organizing your finances doesn’t necessarily mean cutting out all of life’s pleasures or living by counting pennies. On the contrary, it’s about understanding where your money is going, making conscious decisions about your spending and investments, and creating a plan to achieve your goals, whether they are paying off debt, buying a house, taking a trip, or ensuring a comfortable retirement. It’s about having control over your money, instead of being controlled by it.

The Financial Diagnosis: Understanding Your Reality

The first step towards financial organization is to make an honest diagnosis of your current situation. This involves mapping all your income sources (salary, side jobs, investment returns, etc.) and all your expenses. Expenses can be divided into categories to facilitate analysis:

- Essential Fixed Expenses: These occur every month and are fundamental to your survival and well-being, such as rent or mortgage payments, condo fees, utility bills (water, electricity, gas), internet, phone, basic food, transportation to work, and health insurance.

- Essential Variable Expenses: Necessary expenses, but whose amount can vary from month to month, such as groceries (beyond the basics), pharmacy, fuel (beyond what’s needed for work).

- Non-Essential Fixed Expenses: Recurring expenses that are not vital, such as streaming subscriptions, gym memberships, club fees.

- Non-Essential Variable Expenses (Lifestyle): Spending on leisure, restaurants, clothes and electronics shopping, travel, gifts, etc. This is often where the greatest saving opportunities lie.

- Debts: Payments for loans, financing, overdue credit card bills, etc.

There are several tools to help with this mapping, from the good old notebook to electronic spreadsheets (like Excel or Google Sheets) and financial control apps. The important thing is to find the method that works best for you and be consistent in recording. By clearly visualizing where your money is going, you can identify bottlenecks, superfluous spending, and opportunities for adjustment.

The Power of Budgeting: Planning for the Future

With the diagnosis in hand, the next step is to create a budget. A budget is a detailed plan of how you intend to use your money over a specific period, usually monthly. It acts as a guide, helping you direct your resources towards what truly matters and avoid impulsive spending.

One popular and effective method for creating a budget is the 50/30/20 rule, mentioned in our keyword research. This rule suggests dividing your net income (after taxes) as follows:

- 50% for Needs: Essential fixed and variable expenses (housing, food, transportation, health).

- 30% for Wants (Lifestyle): Non-essential spending (leisure, shopping, restaurants, travel).

- 20% for Financial Goals and Debts: Savings, investments, debt payments (beyond the minimum).

It’s important to note that this is a general guideline and may need to be adapted to your reality. If you are heavily indebted, for example, you might need to allocate a percentage greater than 20% to pay off your debts more quickly. If your income is lower, the percentage allocated to needs might be higher than 50%. The key is that the budget is realistic and sustainable in the long run.

The budget shouldn’t be seen as a straitjacket, but rather as an empowering tool. It allows you to make more conscious financial decisions, prioritize your goals, and have more peace of mind about the future.

Setting Clear Goals: The Fuel for Motivation

Organizing finances without clear goals is like running without knowing where you’re going. Financial goals are what give purpose to the effort of saving and controlling spending. They can be short-term (paying off a small debt in 6 months), medium-term (taking a trip in 2 years), or long-term (buying a property, ensuring retirement).

When setting your goals, be specific, measurable, achievable, relevant, and time-bound (SMART method). For example, instead of saying “I want to save money,” define “I want to save $5,000 for a car down payment by December of next year.” This makes the goal more concrete and easier to track.

Break down large goals into smaller steps. If your goal is to save $12,000 in a year, that means saving $1,000 per month. Track your progress regularly and celebrate small victories along the way. This will help keep motivation high.

Getting Out of Debt: A Possible Path

For many, the main motivation for seeking financial organization is the need to get out of debt. Excessive debt can cause stress, anxiety, and negatively impact various areas of life. The good news is that, with planning and discipline, it is entirely possible to reverse this situation.

After mapping your debts (total amount, interest rates, deadlines), the next step is to prioritize which ones to pay off first. Two common strategies are:

- Debt Snowball Method: Pay the minimum on all debts except the smallest one. Focus all extra resources on paying off the smallest debt as quickly as possible. After paying it off, take the amount you were paying on it and add it to the minimum payment of the next smallest debt. The advantage is the motivation generated by quick wins.

- Debt Avalanche Method: Pay the minimum on all debts except the one with the highest interest rate. Focus all extra resources on paying off this debt first. After paying it off, move on to the debt with the second-highest interest rate. The advantage is that, mathematically, you save more money on interest in the long run.

The choice of method depends on your profile. Also, consider renegotiating your debts with creditors. It is often possible to get better payment terms, such as reduced interest rates or longer repayment periods.

Building the Future: Savings and Investments

Financial organization isn’t just about paying bills and getting out of the red. It’s also fundamental to building a solid financial future. This involves creating the habit of saving and, eventually, investing.

One of the first savings goals should be creating an emergency fund. This is money set aside to cover unforeseen events, such as job loss, health problems, or unexpected home or car repairs. Ideally, you should have the equivalent of 3 to 6 months (or even more, depending on your income stability) of your essential expenses saved in a safe and easily accessible investment, such as a high-yield savings account or a short-term government bond.

With the emergency fund established, you can start thinking about investing for medium and long-term goals. Even if you’re a beginner, there are accessible and low-risk options, such as index funds, government bonds, and conservative mutual funds. The important thing is to start, even if with a small amount, and seek knowledge to make more informed investment decisions over time.

Take Control of Your Financial Life

Personal financial organization is an essential pillar for a more peaceful and secure life. It allows you to understand your reality, plan your future, achieve your goals, and have more freedom to make decisions. It’s not a magic formula, but rather a continuous process of learning, discipline, and adaptation.

Start taking the first steps today: conduct your financial diagnosis, create a realistic budget, set clear goals, and begin charting your path to get out of debt and build your wealth. Remember that every small action counts and that the journey to financial organization is a marathon, not a sprint. With information, planning, and persistence, you can take control of your money and transform your life.

This blog, “Debts in Order,” will be here to support you every step of the way, offering information, tips, and tools to help you achieve the much-desired financial health.

Upon us

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been industry's standard.

Popular Post

Leave a Comment